ਲੈਂਡਰਜ਼ ਮੌਰਗੇਜ ਇੰਸ਼ੋਰੈਂਸ (LMI)

ਲੈਂਡਰਸ ਮੌਰਗੇਜ ਇੰਸ਼ੋਰੈਂਸ (LMI) ਦੀ ਮਦਦ ਨਾਲ ਆਪਣੇ ਜਾਇਦਾਦ ਦਾ ਮਾਲਕ ਬਣਨ ਦੇ ਟੀਚਿਆਂ ਨੂੰ ਜਲਦੀ ਹਾਸਿਲ ਕਰੋ।

ਲੈਂਡਰਸ ਮੌਰਗੇਜ ਇੰਸ਼ੋਰੈਂਸ (LMI) ਦੀ ਮਦਦ ਨਾਲ ਆਪਣੇ ਜਾਇਦਾਦ ਦਾ ਮਾਲਕ ਬਣਨ ਦੇ ਟੀਚਿਆਂ ਨੂੰ ਜਲਦੀ ਹਾਸਿਲ ਕਰੋ।

- Home

- About LMI-New-Punjabi

LMI ਕੀ ਹੁੰਦੀ ਹੈ?

ਲੈਂਡਰਜ਼ ਮੌਰਗੇਜ ਇੰਸ਼ੋਰੈਂਸ (LMI) ਇੱਕ ਬੀਮਾ ਪਾਲਿਸੀ ਹੁੰਦੀ ਹੈ ਜੋ ਤੁਹਾਡਾ ਕਰਜ਼ਦਾਤਾ ਆਪਣੇ ਆਪ ਨੂੰ ਉਸ ਜ਼ੋਖਮ ਤੋਂ ਬਚਾਉਣ ਲਈ ਲੈਂਦਾ ਹੈ ਜੋ ਕਿ ਜੇਕਰ ਤੁਸੀਂ (ਘਰ ਖ਼ਰੀਦਦਾਰ) ਆਪਣਾ ਕਰਜ਼ਾ ਮੋੜਨ ਵਿੱਚ ਅਸਫ਼ਲ ਹੋ ਜਾਂਦੇ ਹੋ ਅਤੇ ਤੁਹਾਡਾ ਕਰਜ਼ਦਾਤਾ ਤੁਹਾਡੇ ਵੱਲ ਬਕਾਇਆ ਕਰਜ਼ੇ ਦੀ ਪੂਰੀ ਰਕਮ ਨੂੰ ਵਾਪਸ ਪ੍ਰਾਪਤ ਕਰਨ ਵਿੱਚ ਅਸਮਰੱਥ ਹੁੰਦਾ ਹੈ।

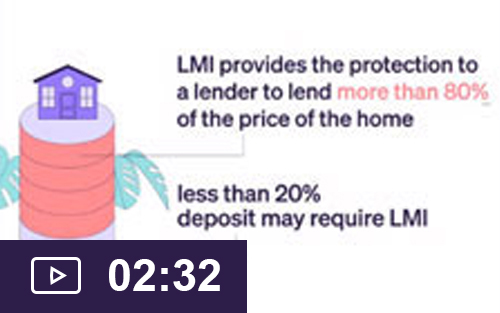

LMI ਉਨ੍ਹਾਂ ਲੋਕਾਂ ਲਈ ਹੋਮ ਲੋਨ ਨੂੰ ਵਧੇਰੇ ਪਹੁੰਚਯੋਗ ਬਣਾਉਂਦਾ ਹੈ ਜੋ 20% ਤੋਂ ਘੱਟ ਡਿਪੌਜ਼ਿਟ ਰਕਮ ਨਾਲ ਘਰ ਜਾਂ ਨਿਵੇਸ਼ ਸੰਪਤੀ ਖ਼ਰੀਦਣਾ ਚਾਹੁੰਦੇ ਹਨ।

LMI ਘਰ ਖ਼ਰੀਦਦਾਰਾਂ ਨੂੰ[1} ਕਿਵੇਂ ਲਾਭ ਪਹੁੰਚਾਉਂਦਾ ਹੈ?

LMI ਘਰ ਖ਼ਰੀਦਦਾਰਾਂ ਨੂੰ 20% ਡਿਪੌਜ਼ਿਟ (ਪੇਸ਼ਗੀ ਰਕਮ) ਤੋਂ ਬਿਨਾਂ ਘਰ ਜਾਂ ਨਿਵੇਸ਼ ਸੰਪਤੀ ਖ਼ਰੀਦਣ ਦੇ ਯੋਗ ਬਣਾਉਂਦਾ ਹੈ, ਅਤੇ ਜੋ ਆਮ ਤੌਰ 'ਤੇ ਜ਼ਿਆਦਾਤਰ ਕਰਜ਼ਦਾਤਾਵਾਂ ਦੁਆਰਾ ਲੋੜੀਂਦਾ ਹੁੰਦਾ ਹੈ।

ਇਹ ਘਰ ਖ਼ਰੀਦਦਾਰਾਂ ਨੂੰ ਹੇਠ ਲਿਖੀਆਂ ਗੱਲਾਂ ਕਰਨ ਵਿੱਚ ਮੱਦਦ ਕਰਦਾ ਹੈ:

20% ਤੋਂ ਘੱਟ ਡਿਪੌਜ਼ਿਟ ਨਾਲ ਹੁਣੇ ਘਰ ਖ਼ਰੀਦੋ

ਪ੍ਰਾਪਰਟੀ ਵਿੱਚ ਇਕੁਇਟੀ ਬਣਾਉਣਾ ਸ਼ੁਰੂ ਕਰੋ

ਵਿੱਤੀ ਭਲਾਈ ਅਤੇ ਸੁਰੱਖਿਆ ਨੂੰ ਮਜ਼ਬੂਤ ਬਣਾਓ

ਕੇਸ ਸਟੱਡੀ: LMI ਦੀ ਵਰਤੋਂ ਕਰਕੇ ਨਿਵੇਸ਼ ਕਰਨਾ

ਇੱਕ ਨਿਵੇਸ਼ਕ $600,000 ਮੁੱਲ ਦੀ ਜਾਇਦਾਦ ਖ਼ਰੀਦਣਾ ਚਾਹੁੰਦਾ ਹੈ ਅਤੇ ਉਸ ਕੋਲ $60,000 (10% ਡਿਪੌਜ਼ਿਟ) ਜਮ੍ਹਾਂ ਰਕਮ ਹੈ।

ਆਮ ਤੌਰ 'ਤੇ, ਕਰਜ਼ਦਾਤਾ 20% ਡਿਪੌਜ਼ਿਟ ($120,000), ਦੇ ਨਾਲ ਵਧੀਕ ਅਗਾਊਂ ਖ਼ਰਚੇ ਦੇਣ ਦੀ ਮੰਗ ਕਰਦਾ ਹੈ।

ਆਪਣੇ ਮੌਰਗੇਜ ਬ੍ਰੋਕਰ ਦੇ ਮਾਰਗਦਰਸ਼ਨ ਨਾਲ, ਨਿਵੇਸ਼ਕ LMI ਦੀ ਵਰਤੋਂ ਕਰਕੇ 10% ਡਿਪੌਜ਼ਿਟ ਨਾਲ ਜਾਇਦਾਦ ਖ਼ਰੀਦਣ ਦੇ ਯੋਗ ਹੋ ਗਿਆ।

LMI ਦੀ ਫ਼ੀਸ ਨੂੰ ਕਰਜ਼ੇ ਵਿੱਚ ਜੋੜ ਦਿੱਤਾ ਗਿਆ (ਪੂੰਜੀਬੱਧ/ਕੈਪਿਟਲਾਈਜ਼ ਕੀਤਾ ਗਿਆ), ਜਿਸ ਨਾਲ ਕੁੱਲ ਕਰਜ਼ੇ ਦੀ ਰਕਮ ਅਤੇ ਕਰਜ਼ੇ ਦੀ ਕਿਸ਼ਤ ਵਿੱਚ ਵਾਧਾ ਹੋਇਆ।

LMI ਨਾਲ ਜਲਦੀ ਖ਼ਰੀਦ ਕਰਕੇ, 20% ਡਿਪੌਜ਼ਿਟ ਜਮ੍ਹਾਂ ਕਰਨ ਲਈ ਉਡੀਕ ਕਰਨ ਦੀ ਬਜਾਏ, ਨਿਵੇਸ਼ਕ ਸੰਪਤੀ ਮਾਰਕੀਟ ਵਿੱਚ ਦਾਖ਼ਲ ਹੋਣ ਅਤੇ ਇਕੁਇਟੀ ਬਣਾਉਣਾ ਸ਼ੁਰੂ ਕਰਨ ਦੇ ਯੋਗ ਹੋ ਗਿਆ।

ਇਹ ਉਦਾਹਰਨ ਸਿਰਫ਼ ਸਮਝਾਉਣ ਲਈ ਹੈ। LMI ਕਰਜ਼ਦਾਤਾ ਦੀ ਸੁਰੱਖਿਆ ਕਰਦਾ ਹੈ, ਅਤੇ LMI ਦੀ ਫ਼ੀਸ ਨੂੰ ਕਰਜ਼ੇ ਵਿੱਚ ਸ਼ਾਮਲ ਕਰਨ ਨਾਲ ਕੁੱਲ ਕਰਜ਼ਾ ਅਤੇ ਦੇਣ ਵਾਲਾ ਵਿਆਜ ਵੱਧ ਜਾਂਦਾ ਹੈ। ਨਤੀਜੇ ਵੱਖ-ਵੱਖ ਹੋ ਸਕਦੇ ਹਨ ਅਤੇ ਜਾਇਦਾਦ ਦੇ ਮੁੱਲ ਡਿੱਗ ਵੀ ਸਕਦੇ ਹਨ।

How much is LMI?

The LMI fee typically charged is between 1% and 2% of the loan amount, depending on the size of the deposit and how much the home buyer borrows.

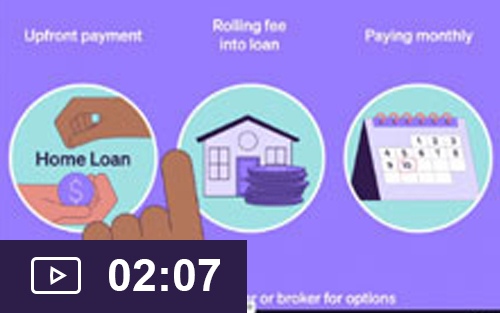

LMI payment options:

- Paid upfront: the LMI fee can be paid upfront as a one-off cost at loan settlement.

- Capitalised into the loan: to reduce upfront costs, the LMI fee can be added to the loan amount and paid over time.

Helia exclusive offering

Family Assistance.

A home buyer may be eligible for a 15% reduction in their LMI fee when it is paid upfront by a family member at the time of loan settlement.

Home buyer’s should speak to their lender or mortgage broker about Helia’s Family Assistance feature.

Home ownership made simple with LMI.

LMI Lets Me In

Find out how more home buyers are using LMI to enter the property market sooner and achieve their home ownership goals.

LMI Lets Me In

Find out how more home buyers are using LMI to enter the property market sooner and achieve their home ownership goals.

Start your home story with LMI.

Discover how LMI helped Mitch and Amelia break free from the rental cycle and purchase their first home with a 10% deposit.

Better, sooner, brighter.

Explore how LMI helped a couple buy a bigger, better property.

What is LMI?

Understand the cost, who it protects and how it can help home buyers purchase a home sooner.

Get home sooner

Struggling to save a 20% deposit? Enter the market sooner with LMI.

LMI Lets Me Invest

Find out how more investors and rentvestors are leveraging LMI to enter the property market now and start building equity sooner.

Frequently asked questions

LMI helps eligible home buyers to enter the property market sooner with a deposit less than 20%, including first home buyers, investors, rentvestors, upgraders and refinancers.

LMI is arranged by the lender to protect them if the home buyer defaults on their loan and the sale of the property doesn’t cover the full amount owing (including loan and sale costs). Any remaining amount is called a shortfall.

By reducing the lenders risk, LMI helps make it possible for home buyers to buy a property with less than a 20% deposit.

LMI has traditionally been viewed as an additional cost to avoid. While it does add to the cost of a home loan, many home buyers are using it as a way to purchase a property sooner, instead of waiting years to save a bigger deposit.

A home buyer may be eligible for a partial refund of the LMI fee paid if the home buyer repays their loan within the first two years.

| Age of policy | Refund percentage |

|---|---|

| Less than a year | 40% |

| 1-2 years | 20% |

Refund eligibility and amounts vary by policy. Refunds don’t apply where repayments are missed or the loan is in default.

Home loan variations

A home loan variation is when a home buyer refinances or varies their home loan with their existing lender.

If the home buyer increases the loan amount only (known as an Additional Advance or Top Up), a new LMI fee is payable. A credit for the LMI fee the lender charged at the commencement of the original loan will apply and the home buyer will need to pay the difference or minimum amount.

If the variation relates to other changes such as replacing the property that is used as security for the home loan, then a limited refund may be payable to the home buyer. The lender will be able to advise if refund options are available.

Financial hardship

If a home buyer is experiencing financial hardship, they should contact their lender early. Solutions are available to help them stay in their home while they navigate a difficult situation.